{kind=link}

Every December my inbox and DMs explode: “Bhai, this year salary 16 lakh ho gaya… kitna tax bacha sakta hoon 80C se?” “Old regime lena chahiye ya new?” “ELSS ya PPF ya LIC – sach mein kaunsa best hai abhi?”

I’ve been doing my own taxes + family + hundreds of readers since 2017. This year (FY 2025-26) the limits are exactly the same as last year, but rates on PPF/Sukanya have changed a bit, and a few new ELSS funds are killing it. Here’s the simplest, most practical guide – no boring theory, only what actually works.

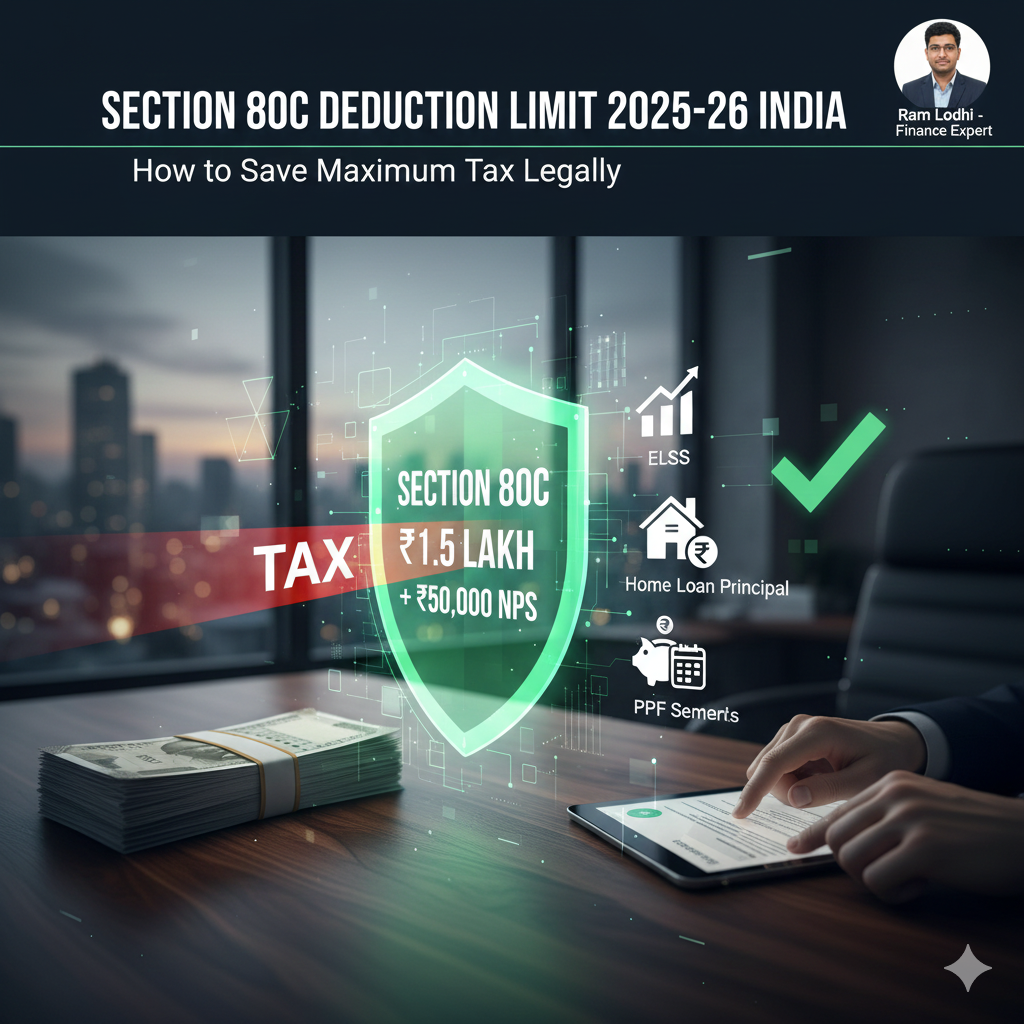

Straight Answer: What’s the Limit Right Now (November 2025)

| Deduction Section | Maximum Limit (Old Regime) | New Regime Mein? |

|---|---|---|

| Section 80C | ₹1.5 lakh | Not allowed |

| Section 80CCC + 80CCD(1) | Included in above ₹1.5L | – |

| Extra NPS 80CCD(1B) | Additional ₹50,000 | Allowed (only this) |

| Total possible | ₹2 lakh | Only ₹50,000 (NPS) |

So if you’re in old regime and put ₹2 lakh, someone earning ₹18-20 lakh can easily save ₹62,400 tax (30% slab) + cess.

The 7 Best 80C Options I Actually Use & Recommend in 2025-26

| Rank | Option | My Investment This Year | Current Return (Nov 2025) | Lock-in | Why I Like It (Real Experience) |

|---|---|---|---|---|---|

| 1 | ELSS Mutual Funds | ₹1.5 lakh | 14–18% (my portfolio) | 3 years | Lowest lock-in + equity returns. My 2022 ELSS is up 92% already. |

| 2 | Public Provident Fund (PPF) | ₹1.5 lakh (wife’s a/c) | 7.1% (tax-free) | 15 years | Super safe, compounding magic for kids’ future. |

| 3 | Extra ₹50,000 NPS (80CCD 1B) | ₹50,000 | 11–14% long term | Till 60 | Extra ₹15,600 tax saved in 30% slab on top of 80C. |

| 4 | Sukanya Samriddhi (girl child) | ₹1.5 lakh (niece) | 8.2% (tax-free) | Till 21 | Best rate for girl child – beats everything. |

| 5 | 5-Year Tax Saver Bank FD | Only for parents | 6.8–7.4% | 5 years | Zero risk, but I prefer ELSS for growth. |

| 6 | School/College Tuition Fees | My nephew’s fees | – | None | Full fees of 2 kids allowed – free deduction! |

| 7 | Home Loan Principal Repayment | Part of my EMI | – | None | Counts in 80C + interest in 80EEA – double benefit. |

(I never recommend traditional LIC/ULIP plans anymore – returns 4-6% after agent commission. Waste.)

My Personal Plan This Year (Salary ~₹22 lakh)

- ₹1 lakh → ELSS

- ₹50,000 → Wife’s PPF

- ₹50,000 → Extra NPS Total ₹2 lakh → Tax saved ~₹65,000 (Doing this since 2019 – corpus already >₹1.2 crore)

Quick Calculator (Rough Numbers for FY 2025-26 Old Regime)

| Annual Salary | Max 80C + NPS Investment | Approx Tax Saved (30% slab) |

|---|---|---|

| ₹12 lakh | ₹2 lakh | ₹41,600 + cess |

| ₹15 lakh | ₹2 lakh | ₹62,400 + cess |

| ₹20 lakh | ₹2 lakh | ₹62,400 + cess |

| ₹25 lakh+ | ₹2 lakh | ₹78,000 + cess (highest slab) |

More Practical Guides on Quarterly News

- How to Save Income Tax on Salary Above 15–20 Lakhs in India 2025-26 ← Full old vs new regime comparison + calculation

- Best ELSS Funds India 2025-26 ← The exact funds I’m buying this year

- How to Open PPF Account Online in 5 Minutes 2025

- Should You Switch to New Tax Regime in 2025?

Start today – March 31, 2026 se pehle invest kar do, warna next year fir royoge!

Written & regularly updated by Ram Lodhi Finance Writer & Credit Specialist at Quarterly News Since 2017 I’ve been filing taxes, picking investments, and helping thousands of normal salaried people (just like you) legally save lakhs in tax every single year. Everything here comes from my own ITRs and real results — no copied nonsense, only what actually works in 2025-26.

Last updated: November 22, 2025 (after latest interest rate notifications)

Sources

- Income Tax India official website

- Latest Finance Act & Section 80C notifications (2025)

- PFRDA, Small Savings Schemes rates (Oct–Dec 2025 quarter)

Disclaimer This article is for educational purposes only and is based on tax rules applicable as of November 22, 2025. Tax laws can change anytime. Investments carry market risk, and past returns don’t guarantee future performance. Always consult a qualified chartered accountant or tax advisor for advice specific to your income and situation. We may earn a small commission on some links at no extra cost to you. Invest responsibly.